At a technology debate held at the Connaught Hotel hosted by Mortgage Solutions and Capita Mortgage Software Solutions, lenders, intermediaries and distributors were invited to talk about the obstacles which remain, and how innovation is seeking to move them aside.

Advancements in mortgage technology have been made but it seems they have yet to revolutionise the mortgage process – but every one knows they will.

The ideal is a digitally joined up housing, mortgage and legal process allowing the consumer to transact in a way which is convenient to them, and in a shorter time frame – but this has yet to be achieved.

A game changing piece of technology, say the attendees, are application processing interfaces (APIs), which allow broker and lender systems to plug in to one another, removing the need to re-key an application into several lenders’ online applications after an electronic fact find has been completed. Achieving this synergy, they say, will do more than cut out repetitive administration – it will cut down processing times by passing the application straight from the broker’s desktop to the underwriter for a decision on the loan.

Close to rollout

Full online integration of APIs in the UK mortgage lending market is being worked on by a handful of stakeholders, although attendees said that behind closed doors a lender is close to rolling out its application-free mortgage process.

The hold up, says one distributor, has been two-fold. First the technology has been slow to develop. It has not been easy to link one system to another. The second barrier has been in the commercial terms which underpin the technology. These have not been agreeable to the firms interested in using APIs. These two factors now appear to be resolved.

One attendee said: “Where we are now is completely different. There are two or three credible organisations with the right commercial outlook which have the technology which can link us together. They may not be able to link 100% of the data on day one, but in the next 12 to 18 months I can see them being able to link 60 to 70% of the data.

A 12 to 18 month wait for a 70% link up of data is too long for some. One attendee said their firm was looking at ways around using APIs until the technology had been fully developed.

Forcing people to get advice

The importance of allowing a home buyer or remortgage customer to transact the way they want to was not disputed by the group, yet some in the room felt the spirit of this was compromised by forcing people to get mortgage advice, regardless of how experienced they were. Technology should empower not force, was one view – the opening up of guidance, rather than advice, was a solution.

Introducing the chatbot

Already a regular feature of many service industries – consumers are used to chasing parcels, discussing faulty goods or arranging a holiday with the use of a chatbot – but can this technology add any value to the mortgage process? One broker was confident chatbots could play an important role in the transaction.

This broker already used a chatbot, called a Digital Mortgage Adviser, which launched in 2016. It uses artificial intelligence to guide customers through mortgage advice, asking questions about their personal circumstances and life events.

“It’s like a Whats App messenger,” said the broker. “You go through that journey with the digital mortgage adviser, it asks you all sorts of questions, and then the chatbot asks the customer if they are ready to chat.” Human mortgage advisers work with the chatbot to step in and provide guidance.

The broker added: “An example of when human intervention is required would be for conflict resolution. If a borrower has asked for the longest fixed-rate possible and then says they want to remortgage in two years, a human needs to step in.”

Chatbots, it was agreed, were more suited to the vanilla market than the complex client market.

An interesting human element emerged from the use of chatbots, said one of the mortgage intermediaries. “We realised we were giving people too much information in one message. We would answer all their questions in one long response. People using the chatbot wanted the impression of humanity in the conversation so we started to break down the responses so they were more conversational.”

A central consumer hub

Most attendees were in agreement that when it came to technology the customer and not the firm creating the tech, was in control.

“The best way is the way the customer wants,” said one guest. Another said: “A good use of technology is being flexible to allow the customer to get what they want from the mortgage process.”

Aside from improving the speed of mortgage advice and process, using tech to create an inviting consumer experience was seen as just as important. “We need an online hub which consumers can click into to find self-help videos, communities of people looking for homes where they can share tips and talk to one another and then a facility which allows the broker to pop up when needed and carry out a Skype interview with the consumer.”

Looking to the future

Looking to the short-term future, six to 12 months, the group were skeptical any major changes would be seen in the market. Open banking was one suggestion, robots which analyse spending habits on bank statements was another. Further down the line winthin five years, significant changes are anticipated.

The definition of the intermediary is expected to change. One attendee said: “There will be two versions of intermediaries: those who offer choice and those who give advice. The two have always gone together until now.”

Another guest added: “There will be lots of changes in the intermediary model if that model is to be effective and competitive. There is talk of one adviser doing 500 to 1,000 mortgages – there will be a lot more efficiencies.”

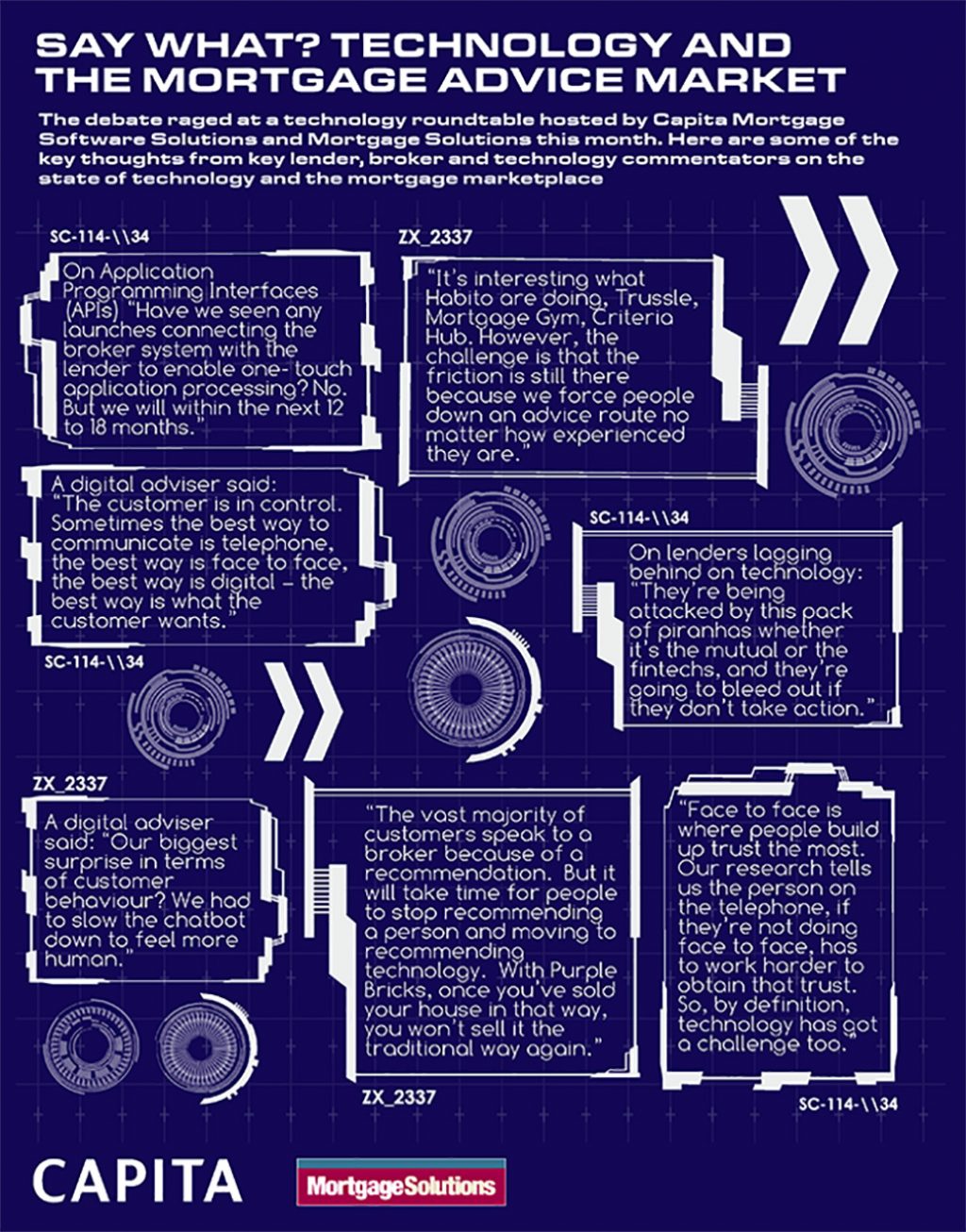

See some of the highlights from the technology debate in our infographic below.