The mutual analysed 10 years’ of Office of National Statistics earnings data and Land Registry house price data for 32 London boroughs and 324 local authorities across England, Scotland and Wales to create calculations of average house price to earnings ratios.

At a national level, since September 2007 affordability has improved by 0.6 per cent in Britain overall, by 18.9 per cent in Scotland, 17.2 per cent in Wales but has worsened by 3.3 per cent in England.

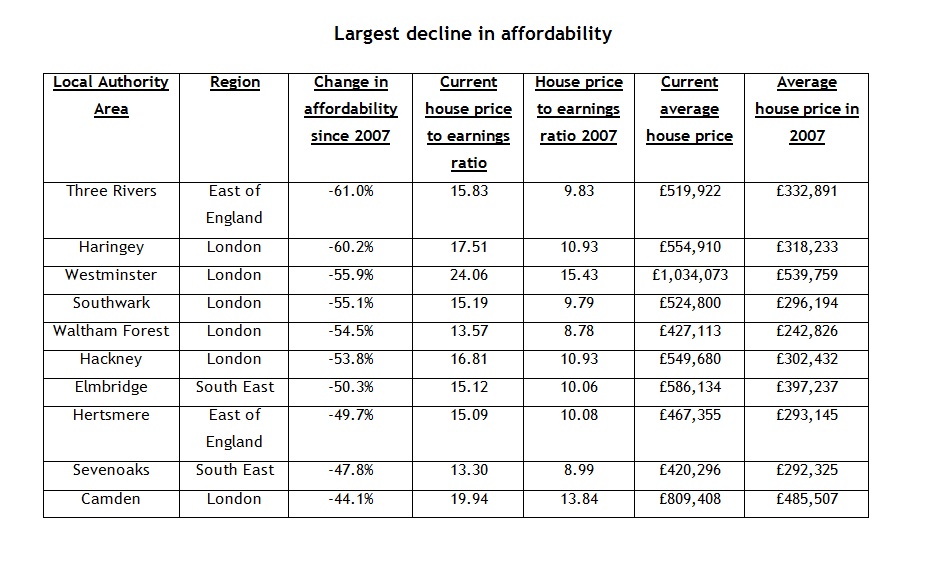

According to the research, homes in London and most of the south of England are now far less affordable than in 2007 as house price rises have outstripped wage growth at a far higher rate. (Click table to expand).

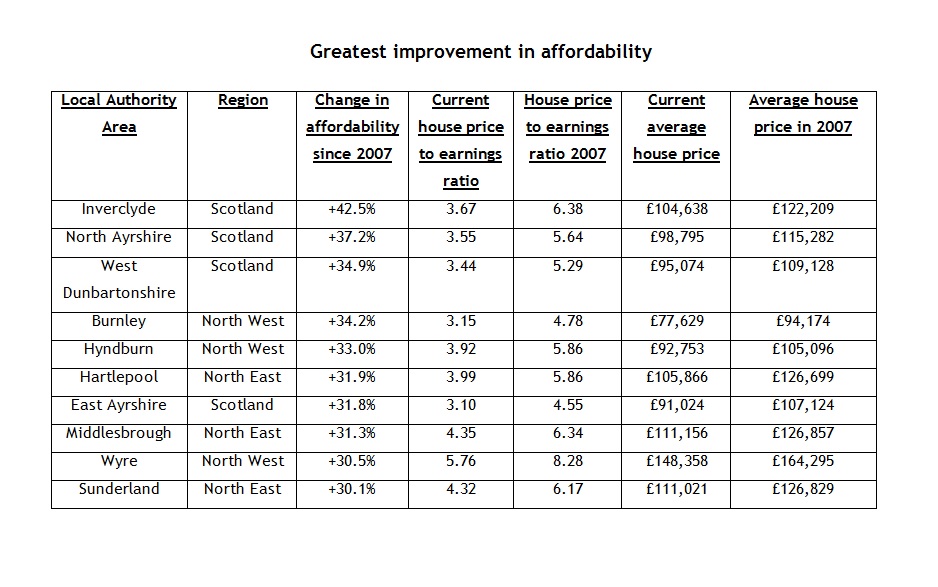

In contrast, homes in 54 per cent of local authority areas – including Edinburgh, Birmingham, Peterborough, Leeds and Harrogate – are apparently more affordable now than before the financial crash due to wages increasing at a higher rate than property values over this period. (Click table to expand).

Andrew McPhillips, Yorkshire Building Society chief economist, said: “Unsurprisingly, the data shows that there is a distinct divide between the north and south of the country when it comes to housing affordability, but this has become even more pronounced since the financial crash.

“Across London and large swathes of southern England, which were already some of the most unaffordable parts of the country, it has become increasingly difficult for first-time buyers and those wanting to move up the housing ladder to be able to buy their first or next home.

He added: “However, the north of England, Wales and Scotland present a different picture entirely, with many places, such as Edinburgh, Peterborough and Birmingham, becoming more affordable than they were before the credit crunch.”

A spokesperson confirmed to Mortgage Solutions that the research did take account of regional disparities in employment levels and earnings. “The data used to work out the ratio for each individual borough was the average wage of a resident in the borough and the average local house price, so it’s a true reflection of the picture in each individual local authority.”

“The only caveat is that the data is derived from PAYE data from the ONS, so it does exclude self-employed and those on benefits, but is the most accurate reflection of income we could find.”

Regional changes since 2007

The research shows affordability has worsened most dramatically for London borrowers, where buying the average home is now less affordable in every borough than it was before the credit crunch, dropping on average by 39%. Council areas in the South East and the East of England have also seen a significant drop in affordability, with homes on average becoming 15% less affordable to buy.

The biggest improvements in affordability have come in the North East of England where affordability has increased by an average of 26 per cent, followed by Scotland (20 per cent), Wales (18 per cent), the North West (16 per cent), and Yorkshire and the Humber (14 per cent).

The Three Rivers council area in Hertfordshire and Haringey in north London saw the biggest declines in affordability since the economic crisis, with homes becoming 61 per cent and 60 per cent less affordable to buy over the past 10 years. Average house prices in these authority areas have increased to £519,992 (a £187,101 rise) and £554,910 (a £236,677 rise), respectively.

The average home in Three Rivers now costs 15.83 times the average salary, with this figure at 17.51 in Haringey. The least affordable place in Britain is now Westminster, where a home costs 24.06 times the average wage.

By contrast, Inverclyde, near Glasgow in Scotland, saw the country’s biggest increase in affordability, with homes now 42% more affordable than in 2007 and costing 3.67 times the average salary, followed by North Ayrshire, where homes are 37% more affordable 3.55 times the average wage.