New homeowners are turning to longer mortgage terms as they ditch the traditional 25-year mortgage term.

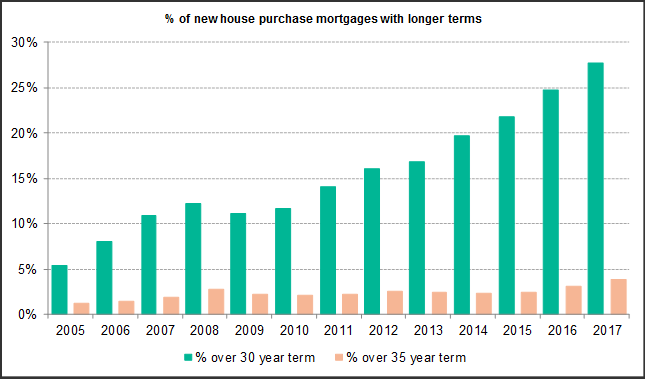

Data from UK finance revealed that in 2017, around 27% of all new homeowners took out 30-year mortgage terms while 4% took out 35-year terms.

In fact, the trend for longer mortgage terms has been on the up since 2009, having risen steadily from the 11% of 35-year mortgage terms recorded during the financial crisis.

Going back further, UK Finance found that in 2005, 6% on new house purchase mortgages were on a 35-year term.

Pros and cons of longer mortgage terms

Longer mortgage terms tend to have lower monthly repayment option, which provides people with an affordable route to homeownership.

A UK Finance spokesperson, said: “This demonstrates how providers are lending responsibly and making sure borrowers can afford their mortgages.

“Most mortgage products also allow early and increased repayments or overpayments, giving customers the flexibility to manage their finances and adapt to new circumstances.”

However, Rachel Springal, finance expert at data site Moneyfacts, said opting for a longer mortgage may seem like a good idea on outset, but borrowers will ultimately repay more in interest.

She said: “Borrowers will find that the monthly repayment can be more manageable than if they opted for a shorter mortgage.

“However, lowering the monthly repayment does not lower the overall cost of your mortgage, as you end up paying out more in interest due to taking longer to repay the debt (as interest is charged on the borrowed sum until it is repaid).”

Springall suggests that the best course of action for new borrowers is to get a couple of quotes for the mortgage before applying, such as a 25-year mortgage term versus a 30-year mortgage.

“At this stage, both the monthly repayment and the overall cost of the mortgage should be compared. If borrowers can stretch their cash it’s worthwhile to pick a shorter deal and also to consider overpaying to shorten the term even further.

“As always, it’s worth seeking independent financial advice to help navigate the mortgage minefield,” she added.