Nationwide re-joined stalwart lenders such as HSBC to offer 90 per cent deals last month, exclusively for first-time buyers, with an additional condition.

Buyers will need to prove that at least 75 per cent of their deposit has come from their own savings, ruling out deposits that have been gifted entirely from parents.

If the source of the deposit is an inheritance it will be counted as coming from the borrower’s own savings.

A Nationwide spokesperson said: “Nationwide is currently the only major high street provider to return-to 90 per cent lending for first-time buyers without any volume restrictions.

“These are difficult times for those looking for their first home and affordability must be placed at the forefront of any decision.

“As we outlined at the time, we will accept gifted deposits up to 25 per cent of the total value, however, we ask that the majority comes from the mortgage applicant as it demonstrates that someone is able to save and manage their finances.

“Above all we need to continue to lend responsibly as we consider how we can help people move home at this uncertain time.”

More deals coming

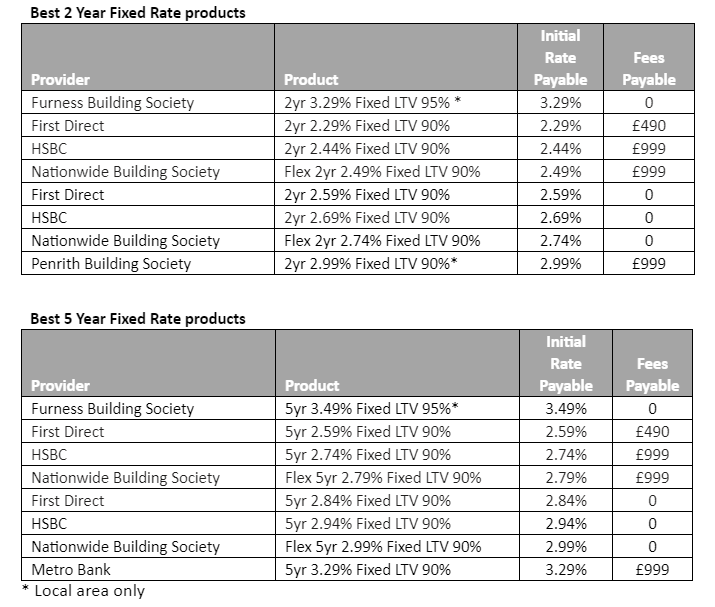

There are now 28 fixed rate deals available to buyers with a 10 per cent deposit, according to analysis by ratings service Defaqto.

Since Chancellor Rishi Sunak delivered his summer statement on 8 July, ten fixed deals have been launched. However, small building societies such as Furness and Penrith restrict their high LTV lending to their local areas.

HSBC, which has maintained its decision to support high LTV lending throughout the pandemic, has put in place daily lending limits to control volumes.

Sunak’s stamp duty holiday, also revealed in his summer economic plan, will help first-time buyers living in areas of the country with expensive housing, but it has also created more competition for the traditional starter home.

Buy-to-let investors will benefit from the stamp duty break but will continue to pay the three per cent stamp duty surcharge.

Katie Brain, insight analyst for banking at Defaqto, said: “It can be really hard to save for a deposit for a home and high LTV mortgages are often the only way a first-time buyer can get on the ladder.

“The stamp duty holiday may help first-time buyers but without the finance, home-ownership will be out of reach for most.

“It is encouraging to see lenders returning to the market and new products coming out for those with small deposits. We are seeing many come onto the market for only a few days and so borrowers will need to act quickly to secure these deals.”

Source: Defaqto