Speaking to Mortgage Solutions, head of BM Solutions Phil Rickards (pictured) discusses why he has held back from entering the market, the impact of a large lender’s presence and why traditional buy to let still needs a champion.

Speaking to Mortgage Solutions, head of BM Solutions Phil Rickards (pictured) discusses why he has held back from entering the market, the impact of a large lender’s presence and why traditional buy to let still needs a champion.

BM has been monitoring the market for well over a year, judging if and when it may be right to offer buy-to-let mortgages through a company structure; the market will have to wait a while longer before it gets a decision.

“It’s something we may need to consider as the market continues to evolve,” said Rickards. “Our immediate priority is to work through the upcoming Prudential Regulation Authority (PRA) minimum standards for portfolio underwriting to ensure that we continue to write quality business in a compliant manner.”

Does the market need heavy weights?

Several concerns sparked calls for BM or The Mortgage Works to begin lending to limited companies. Some in the sector worry that lenders offering the products will buckle under the weight of applications, and be unable to offer an efficient service. Others feel the presence of one of the two lending giants would raise the market’s profile, helping it to grow and evolve. Rickards sets the record straight.

“it’s a matter of opinion as to whether the market’s profile needs to be raised”

He said: “Undoubtedly the presence of BM, or any other major lender for that matter, would help to raise the market’s profile but it’s a matter of opinion as to whether the market’s profile needs to be raised.”

BM has already taken to the road to explain the consequences of the tax changes to over 8,000 brokers and Rickards is not convinced that a volume lender is the answer to brokers’ service-level worries.

“I’m sure we would be able to bring some of the service level efficiencies for which we have become well known,” he said.

“However, it’s important to remember that there are different considerations for this form of lending, particularly when landlords are building portfolios which are likely to fall within the new PRA standard. Any of the traditional service benefits as we know them, may well be outweighed by additional underwriting requirements and increased paperwork.”

A captive audience

Kent Reliance saw its proportion of limited company lending, as a percentage of overall lending, rise from 40% to 57% last year.

Kent Reliance saw its proportion of limited company lending, as a percentage of overall lending, rise from 40% to 57% last year.

While this gives the impression that demand is rising, it could be argued that Kent already has a captive audience of professional landlords suited to products of this kind, and the tax changes have naturally driven them to switch from individual ownership to limited company.

Whether it will become the preferred method of holding property among small-scale landlords remains to be seen.

“Taking into account the amount of change the market has gone through in the last 12 months, buy to let is clearly becoming segmented. Limited company is just one segment.”

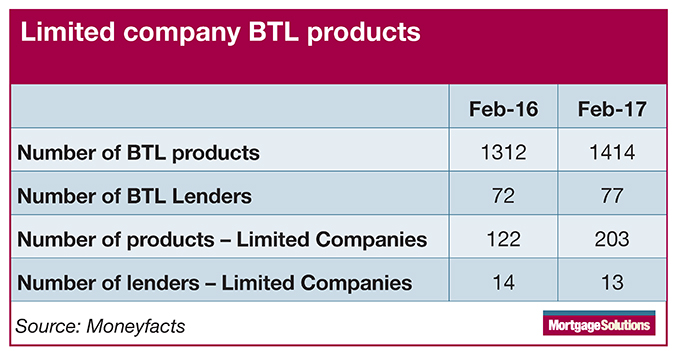

The actual market is hard to gauge because the Council of Mortgage Lenders does not keep tally of how much lending is advanced through limited company structures. However, the hype around Ltd Co in the run up to the April tax changes may lead spectators to believe the size of the market is bigger than it is.

Rickards estimates limited company accounts for around 10% of the market. “There are a number of specialist brokerages who appear to be set up for this form of advice and are clearly promoting it as a viable option,” he continued.

“Taking into account the amount of change the market has gone through in the last 12 months, buy to let is clearly becoming segmented. Limited company is just one segment.”

Basic rate taxpayers

Rickards said that traditional buy to let, lending to individuals, still accounted for the majority of business being written. Many will remain basic rate taxpayers after the changes to tax relief for landlords have been applied, making the traditional arrangement of owning investment properties in an individual name a viable option for many.

Rickards added: “All of that said, it has never been more important for customers to seek specialist tax advice before entering into a BTL arrangement and for brokers to really understand a customer’s long-term goals and aspirations so that they can match the correct mortgage arrangement to those aspirations.”

You may also be interested in the Mortgage Solutions newsletter. All the latest news, analysis and insight from the mainstream residential lending market. Including industry news, adviser business strategy tips and market commentary.

You may also be interested in the Mortgage Solutions newsletter. All the latest news, analysis and insight from the mainstream residential lending market. Including industry news, adviser business strategy tips and market commentary.