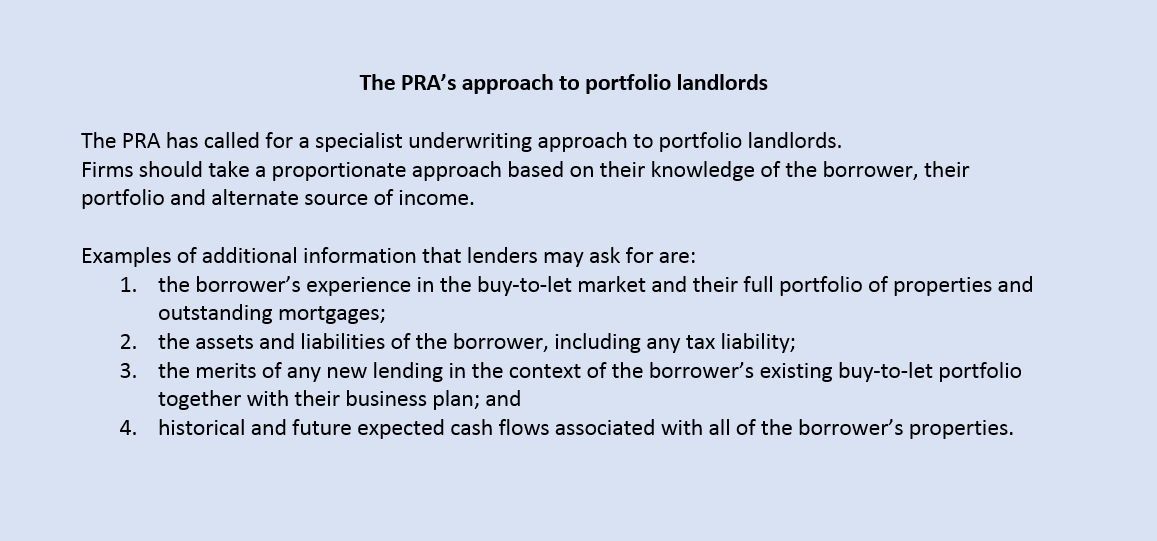

Lenders offering buy-to-let mortgages to landlords with four or more mortgaged properties in their portfolio will be subject to a stricter set of underwriting rules from 30 September (see graphic below).

As yet, no lender has shown its cards and the atmosphere in the broker market is becoming restless.

Specialist Lending Solutions spoke to three buy-to-let specialists and asked: “What do you need to know from lenders about their new portfolio landlord requirements, and by when?” While all three firms discussed different requirements, one message resounded unanimously, “tell us by the summer”.

Who is in the running

Not only are brokers in the dark about the shape of the proposition they will be dealing with, although many point to Paragon as the template, they don’t know who will be operating in this space come October.

Jane Simpson, managing director of TBMC, said lenders needed to start coming clean about whether they intended to back out of this market and drop their maximum property limit to three.

How lenders judged the size of the portfolio, to establish if it would be subjected to the tougher underwriting requirements was another of Simpson’s queries. She wants to know if different lenders will apply different rules which would tip one landlord into the realms of portfolio lending, while another would not.

“I want to know if it will be as simple as counting each property, or if the size of the portfolio will be judged on other factors, for example, will properties below a certain loan-to-value be discounted?” she said.

Criteria queries

Loan-to-value and debt servicing requirements are an obvious must, but brokers want to be clear on whether lenders plan to follow the current route of 125% rental cover for limited companies and 140 – 145% for individuals.

The issuing of stress-testing raised multiple questions among intermediaries, and crystal clear guidelines are called for in this area. For example, will two stress test calculations be carried out, one on the whole portfolio and one on the subject property? If so, at what levels?

The benefits of taking a five-year fixed rate mortgage is also of interest. Brokers want to advise their clients on how to get the maximum leverage from their portfolio.

Document requirements

Steve Olejnik, head of sales at Mortgages for Business, is hoping for a common sense approach to evidence gathering and has a few suggestions.

Rather than ask for mortgage statements for each property, Olejnik hopes lenders will request a property schedule which outlines the mortgage balance, valuation, rents and mortgage debts. The balances can be checked against the credit report.

He wants to see lenders exercise a tolerance of how many balances need to be proven. “It would be good to know if lenders are happy to have 80 or 90% of the portfolio evidenced, and waive 10% for the balances which are not showing on the credit file. This will be far more time efficient than asking for mortgage references or statements on missing balances,” he added.

A unified approached to cash flow forecasting is also on the wish list. Olejnik said: “It would be great if all lenders adopted a unified method of proving cash flow. I would like to see lenders ask for bank statements to verify the rent coming in and the mortgage going out, rather than asking landlords to put together a detailed cash flow document.”

Guidance on any unusual information expected on a business plan is welcome. Typically, said Olejnik, a business plan would consist of the landlord’s future purchase plans, how the landlord manages the portfolio and the investment strategy.

Stance on income discrepancy

There is concern that if tax returns are requested as proof of income, they may not match the actual rent being received. Brokers want guidance on how the lender expects them to handle this. Intermediaries want clear explanations of how much tolerance, if any, the lender will give before they class it as reportable event, and start calling it fraud. “What responsibility does the lender expect the broker to take in the reporting of income discrepancies?” asked Olejnik.

Valuations

Valuation requirements are a big question mark. Brokers want to know if any background properties will need a full valuation or an AVM, or whether lenders will be doing their own research on websites such as Zoopla and Right Move.

Lender training sessions

The call for summer announcements was echoed by Olejnik, Simpson and Paul Atkinson, head of mortgages at Finance 4 Business.

Atkinson said it was important they were not left in the dark and given at least six weeks notice, which would give them time to get up to speed with each lender’s policy.

Simpson wants lenders to offer training. “I’d like an underwriter from each of the lenders to come and sit with us and go through a case,” she said.

“Of course it is important to know what the lender needs in order to underwrite the case, but it is also crucial to know why. If that is not possible, let us send our senior processors to the lenders’ offices for a day’s training.

“If we get the information we need by the start of August, when business tends to be quieter, we can use that time to up skill our teams on the processes and be in a strong position to advise our members on the new requirements.”

You may also be interested in the Mortgage Solutions newsletter. All the latest news, analysis and insight from the mainstream residential lending market. Including industry news, adviser business strategy tips and market commentary.

You may also be interested in the Mortgage Solutions newsletter. All the latest news, analysis and insight from the mainstream residential lending market. Including industry news, adviser business strategy tips and market commentary.