The challenge

The client came to us in straitened circumstances.

They required stock which was supplied to a range of clothing outlets including household names such as TK Maxx. Any funding would only be a short-term fix for two-to-four months, which ruled out term lenders.

The firm’s credit profile wasn’t ideal by their own admission, but without an immediate cash injection to buy more stock, the client would face the possibility of losing more revenue.

They were using an inhabitable property as security, but no conventional lender would agree.

And personal loans would put a strain on cashflow which was already an issue as the business was a main source of personal income.

However, the valuation fee of the very large three-storey seafront property came in higher than the client expected, at around £980,000.

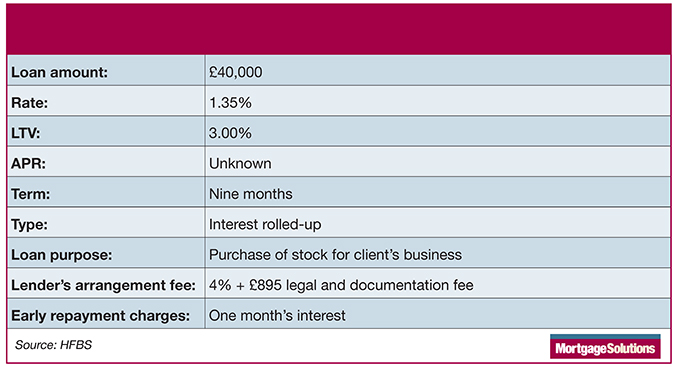

The deal

The solution

We used the applicant’s main residence as security by way of a second charge, which was secured following a meeting between the lender and client.

The deal was completed in nine working days and allowed the client to purchase stock for their business and meet their supply contract.

Ian Broadbent, director at Holme Finance Bridging Solutions explains why they were happy to take on the loan: “The client had been left in an embarrasing set of circumstances which were beyond his own control.

“He was able to provide evidence that he would be in a position to rectify the situation very shortly but had he failed to meet the demands of an upcoming contract with some big high street names, it could potentially have resulted in the demise of his entire business.

“With just a small short-term loan to assist with cash-flow, we enabled the client to continue to earn. While the property was currently not habitable, we were able to evidence a significant value and as such we were able to proceed without the need for a full valuation.”

You may also be interested in the Mortgage Solutions newsletter. All the latest news, analysis and insight from the mainstream residential lending market. Including industry news, adviser business strategy tips and market commentary.

You may also be interested in the Mortgage Solutions newsletter. All the latest news, analysis and insight from the mainstream residential lending market. Including industry news, adviser business strategy tips and market commentary.