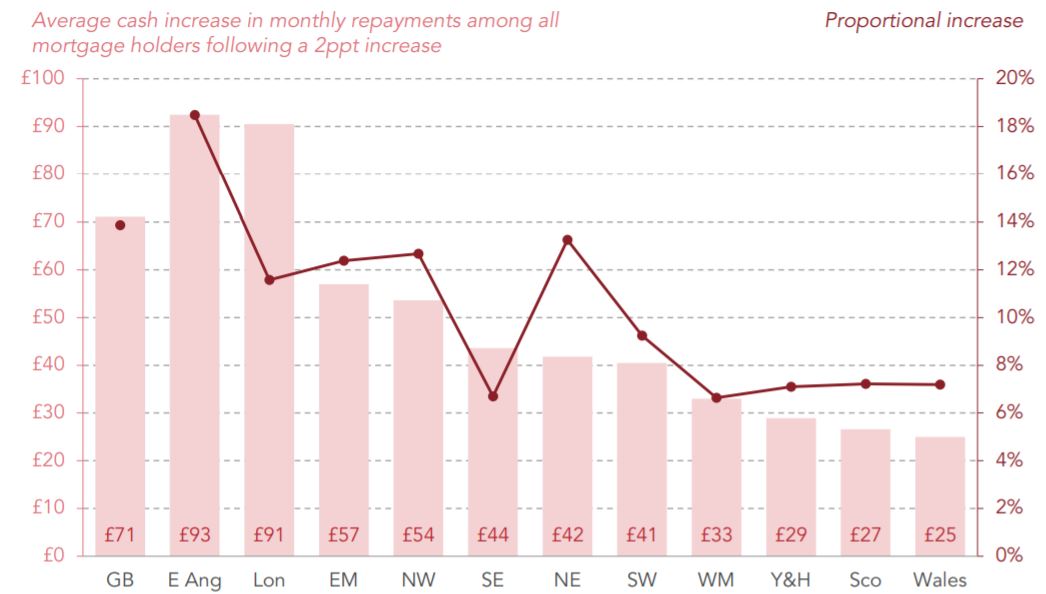

A 2%-point increase in mortgage rates would raise the typical monthly repayment by £71 a month, according to the study.

But homeowners in East Anglia and Greater London would see average rises of more than £90.

In contrast, those in Wales and Scotland would see a typical repayment increase by less than £30.

On an age basis, homeowners aged 25-34 would potentially see bigger rises, with payments rising by an average of £88.

Mortgage bills among those aged between 55 and 64 would rise by a typical £37.

But the hardest hit would be low income and so-called mortgage prisoners, who no longer satisfy borrowing criteria, warned Resolution.

It comes as mortgage rates are expected to rise in the coming months, with another base rate increase potentially coming from the Bank of England as soon as May.

The end of the Term Funding Scheme (TFS) this month, which gives banks and building societies cheap money for lending, could also push up mortgage bills.

Low income families most at risk

Debt distress is already a reality for significant numbers of lower income households, and policymakers must remain sensitive to the worrying prospects faced by many indebted families, Resolution said in the report.

In the event of two percentage point increase to mortgage rates, homes at risk, classed as those spending 30% or more of pre-tax income on a mortgage, would rise from 12% to 15%.

But among families in the lowest fifth income homeowners, those at risk would rise from 57% to 59%.

The biggest jump in those at risk would be for mortgagors in the second quintile of income, rising from 17% to 26%.

Among mortgagors in the top fifth of income distribution, the proportion at risk would rise marginally from 4% to 5%.

Mortgage prisoners, with little option but to remain on their current lenders’ standard variable rate (SVR), could see steep increases in bills – because the rate often reacts quickly to an increase in the base rate, the report added.