Better Business

FCA permissions: Know the bigger picture to avoid the pitfalls

Knowing which regulatory permissions your firm needs to conduct business is not enough to avoid landing in hot water, writes Samantha Partington.

Understanding the activities of those businesses higher up and further down the supply chain is just as important.

Three regulatory pressures circle broker firms in the intermediary sector, all coming home to roost in March next year, bringing with them their own individual complexities.

The Financial Conduct Authority (FCA) took over control of the consumer credit industry in April 2014. Anyone holding a credit licence granted by former masters the Office of Fair Trading (OFT), for example buy-to-let and bridging brokers, needed to reapply to the FCA to trade under a new credit regime by 31 March 2016.

Running in tandem to this are the demands of the Mortgage Credit Directive (MCD) which must be met by 21 March. The MCD requires firms carrying out regulated second-charge business to become approved for advising on regulated mortgage contracts. Throw into the pot authorisation for firms wishing to deal with consumer buy-to-let applications and the paperwork mounts up.

Initially firms were bamboozled by the variance in the permissions they needed but with less than six months to go it seemed the industry had got to grips with what was required of them.

Aldermore Insights with Jon Cooper: Edition 9 – Why lending strategy is becoming more central in buy to let

Sponsored by Aldermore

But after attending a workshop held by Connect Mortgage Club, hosted by director Liz Syms, Mortgage Solutions found there was still a surprising number of areas which intermediaries remained unaware of.

Lenders going beyond the letter of the law

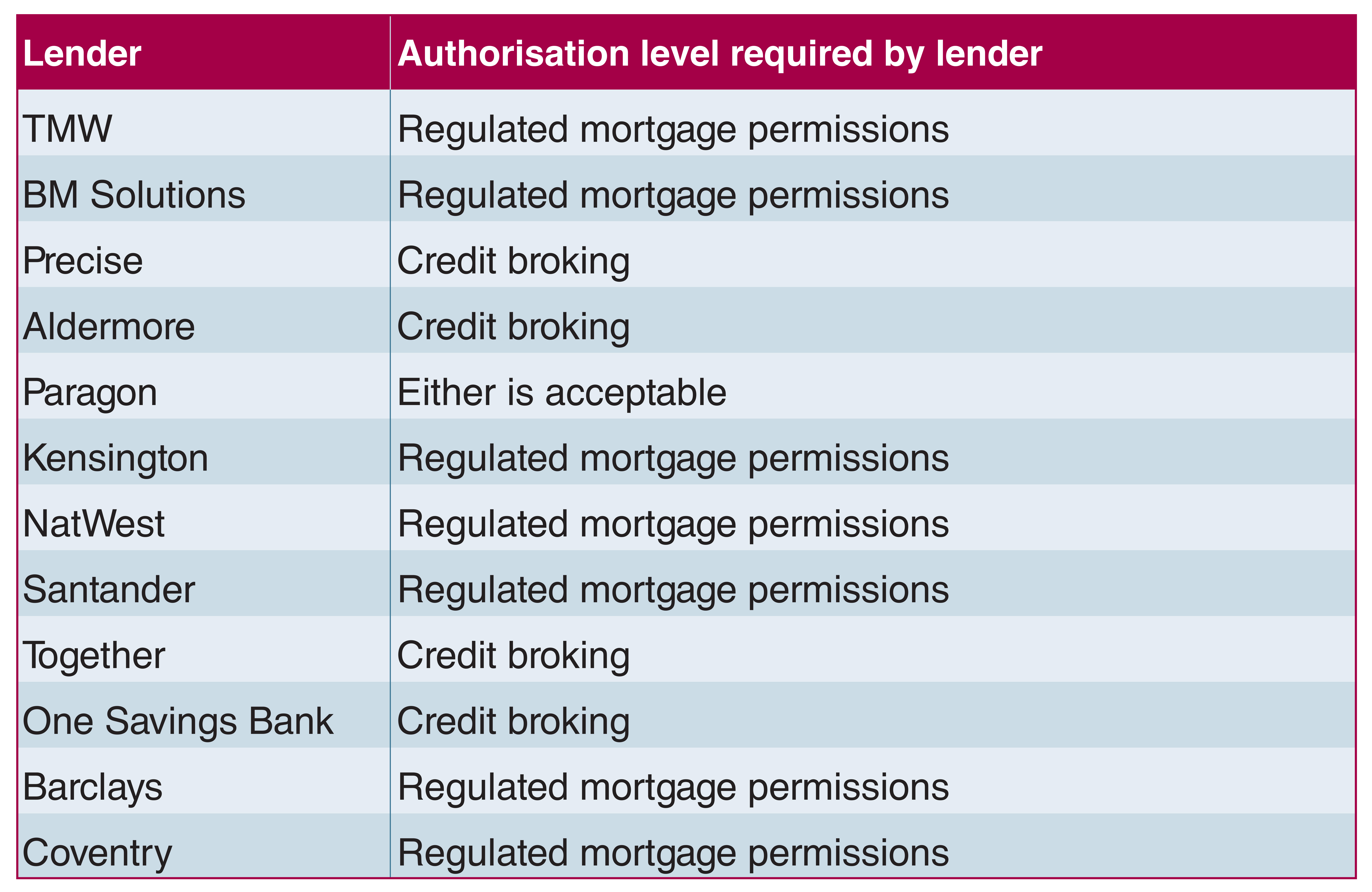

To advise and arrange on buy-to-let business, intermediaries will need permissions for credit broking to comply with the FCA’s requirements but many lenders are insisting on more.

Syms says that most of the larger buy-to-let lenders are only working with brokers who have regulated mortgage permissions; a step beyond what the regulator demands. She says brokers who have applied for credit broking permissions only may want to consider upgrading to make sure they have access to the whole buy-to-let market.

Know your introducer’s permissions

Mortgage brokers will not have been faced with the same level of administrative leg work as their second-charge counter parts. Already in possession of permissions to advise on regulated mortgages they will only need to top up with debt counselling for remortgage applications. But, the origins of mortgage leads could pose a threat to intermediaries. Brokers accepting introduced business from any introducer that does not have the correct permission under the FCA, risk fouling fall of the regulator.

Syms warns brokers not to be complacent, some introducers may not have reapplied when the FCA took over from the OFT but may continue to refer business illegally. It is becoming more common for lenders to ask about the permissions of the introducer, says Syms, so intermediaries need to know where to look to find out if the firm is permitted to make introductions and what variances in the permissions mean. The FCA has a search facility which allows brokers to check up on firms introducing business to them.

As the definition of credit broking includes introductions to other brokers most introducers will need to have credit broking permission. The FCA gives a full breakdown of credit broking in its handbook PERG 2.7.7E G01/04/2014. This allows introducers to pass on any finance lead to an intermediary.

The regulator has also offered introducers the option to apply for limited credit broking permissions which is a cheaper and quicker application process but is not sufficient cover for all. If your introducer has limited credit broking permissions, credit broking must be a secondary business for them. Introducers which fall into this category, for example, are car dealers referring a customer for finance or accountants and solicitors referring customers who have asked for financial guidance following a legal transaction.

Permission pitfalls

There remain some question marks over certain introductions which Syms refers to as ‘grey areas’.

Her warning to brokers is to be careful accepting introductions in an informal setting. Taking recommendations from a ‘mate down the pub’ as a one-off will probably not constitute credit broking but regular referrals from a builder might. Business referred to brokers at networking events arranged, for example, by the British Network International, would likely to be interpreted as ‘by way of business’ so the broker would need to check if the networking host holds permissions for credit broking. Syms says whether these types of introductions class as credit broking boils down to a piece of small print in point three of the six activities listed for credit broking;

‘effecting an introduction of an individual who wishes to enter into a credit agreement or a consumer hire agreement to a person who carries on an activity in or by way of business’.

‘By way of business’, says Syms, implies that the person passing on the lead will in some way be compensated for the introduction. This is not the case. Even if no payment is made for the introduction, this activity will be seen as credit broking by the regulator regardless of the setting and the introducer will need credit broking permissions authorised by the FCA.

So whatever the shape of your business or future plans, make sure you don’t get caught out in your current business practices or further down the line.