Better Business

Case study: Purchasing a buy to let with a special purpose vehicle

Guest Author:

Mortgage SolutionsJames Jenkins, broker at Axis Finance (pictured) approached Mortgages for Business to help source specialist buy-to-let finance for his clients, a family who were looking to purchase properties via a special purpose vehicle (SPV) limited company.

The clients

The family comprises both parents and two adult children, all in full-time employment. The parents own a construction company and are both experienced landlords, with a large portfolio of 17 rental properties held in their personal names. Due to the changing tax environment they had decided to make all future buy to let purchases via a limited company and have recently set up a Special Purpose Vehicle with themselves and their children as the four directors.

Commenting on their decision the husband said: “My wife and I have built up a substantial property portfolio over the years and have always purchased property in our personal names. However, the Chancellor’s Summer Budget really made us rethink our buy to let strategy going forward. As higher rate tax payers we knew the proposed restriction to buy to let interest relief would have a huge impact on our finances.

We contacted our accountant who showed us the figures and it became clear that setting up an SPV really was the only way forward if we wanted to continue as property investors.”

The properties and whether to purchase personally or via an SPV

Two five-bed houses in a well-known Southeastern university town to be let to students. Total purchase price £523,000.

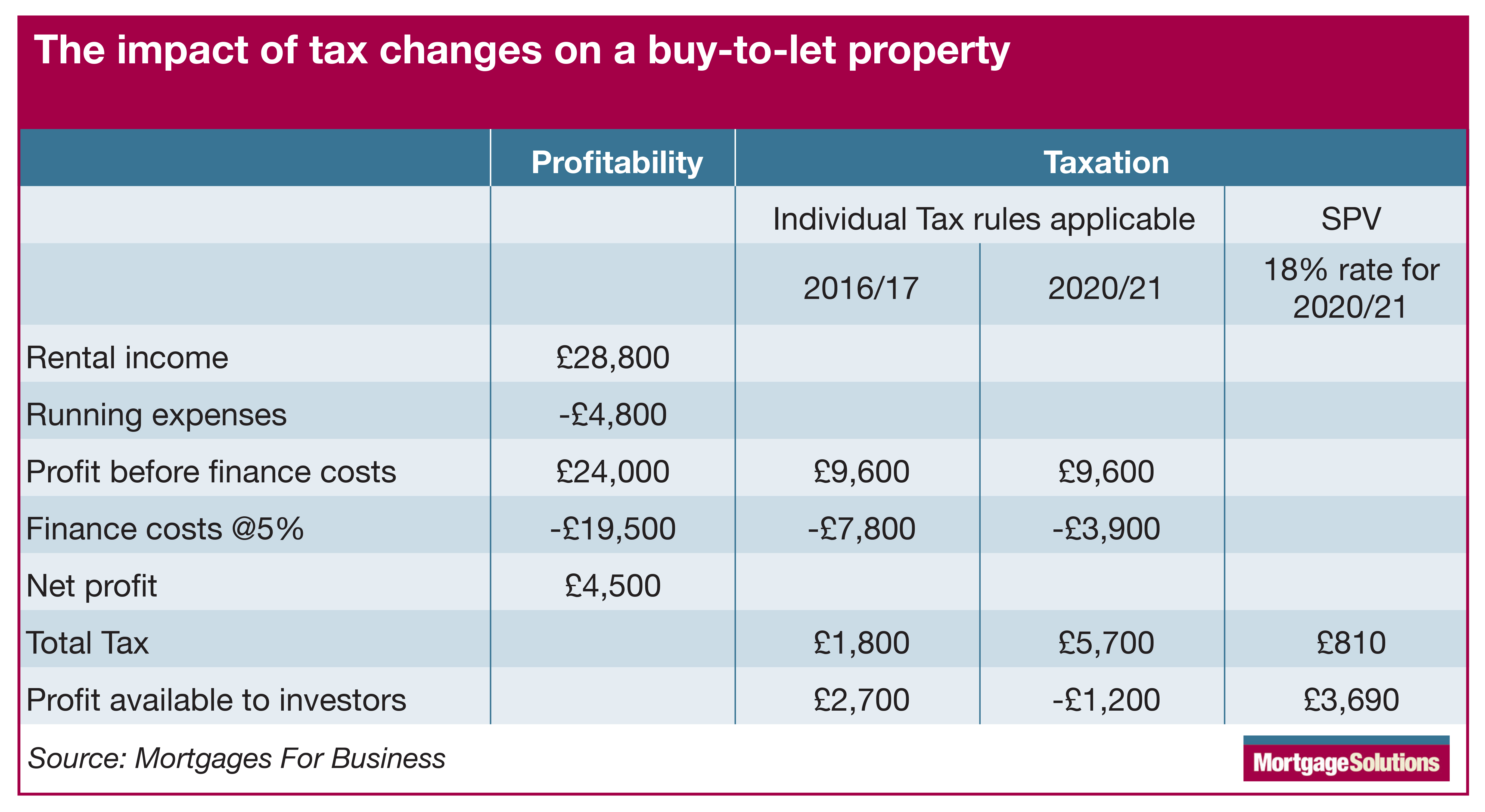

With the two properties each yielding a rent of £1,200/month the family had anticipated raising a 75% mortgage (£390,000) at a cost of around 5% pa and making an overall profit after expenses and interest of around £4,500 (before allowing for any potential gain in the value of the property). This all changed in July when the Chancellor decided to restrict deductibility of finance costs for individual BTL investors – starting in April 2017 and with full effect from April 2020.

The impact of the tax changes on individual purchasers of BTL properties paying tax at 40%, and of the decision to buy in an SPV, are shown in the table below:

Thus the family had the intolerable prospect that by 2020/21 their Income Tax bill relating to the rental of these properties could exceed their profit from them. Through using a limited company they have avoided this problem – although there is added complexity and additional tax to be paid in order to take the after tax profit out of the SPV. Each shareholder will have a different situation depending on their other income and in particular the extent of other investment income. However, with the first £5,000 of investment income free of additional tax for each individual, there is the possibility that individual shareholders will not suffer any further Income Tax on this income.

Whilst there were some additional costs incurred these were small in comparison to the potential tax savings. Additional costs included:

- Solicitors fees – for limited company applications both the client and the lender need separate legal representation, so two lots of solicitor’s fees must be paid

- Increased arrangement fees – limited company applications involve more underwriting, so costs are slightly higher

- A guarantee is asked from all directors

The challenge in finding a lender

The deal was quite complex – James Jenkins needed to find a lender for his clients that would accept:

- A newly established SPV limited company

- Clients with a large portfolio (17+ rental properties)

- Clients with multiple sources of income

- Clients with links to developments

Both the clients and James were also hoping for a quick turnaround time as the mortgage adviser explains: “My clients’ situation meant that placing the deal wasn’t going to be a straightforward task. I knew the application was not mainstream and that I would need to use one of the specialist lenders. I researched numerous lenders’ pricing and criteria and decided that in this case, Keystone would be the best fit.

“Keystone is the lending brand of Mortgages for Business and they have a lot of experience of limited company applications for both SPVs and trading businesses. I have a strong relationship with the underwriters and the management team, and their processing is pretty fast. From past experience, I know I can pick up the phone and speak to the specific underwriter working on the case and get answers to important questions that allow me to manage my client’s expectations.

I was right, the team at Keystone rapidly grasped all the technicalities which helped the case progress quickly.”

The deal

The application was submitted in December and offered on 15 January. The case is expected to complete within the next month, so that the clients avoid the further expense of a 3% surcharge on Stamp Duty which comes into effect on 1 April 2016.

Subsequent to this application being submitted James has submitted a further application for the same clients to Keystone, which is also due to complete before 1 April.

The client said: “We are so thankful that our broker and accountant were able to send us in the right direction – saving us time and money.”

With thanks to Mortgages for Business.