The challenge

The client wanted to purchase a semi-commercial property as an investment. The property was a low-value building with a newsagent on the ground floor and a one-bedroom flat above.

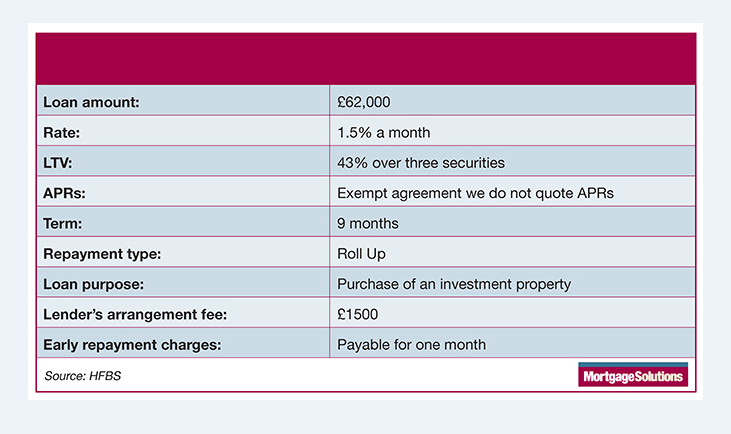

Due to the low value of the property, £62,000, many lenders would have considered this to be unmortgageable.

A lender was identified to finance the deal but this would have taken a couple of months to get to the completion stage. The sale was agreed on the understanding it would be completed within 28 days.

The deal

The solution

Only one mortgage lender would consider this deal and would have taken too long, so we turned to the bridging market.

I approached bridging lender HFBS to finance the deal within the timeframes, which it secured against three properties. The client was able to offer the new semi-commercial property as security as well as two low-value standard residential properties (worth £40,000 each).

HFBS met with the client at his home address to discuss requirements, needs and future plans.

A full commercial valuation on the new purchase was required but we were able to rely on drive-by valuations for the two residential properties as they were both standard two bed mid-terraced houses – this kept upfront costs to a minimum.

You may also be interested in the Mortgage Solutions newsletter. All the latest news, analysis and insight from the mainstream residential lending market. Including industry news, adviser business strategy tips and market commentary.

You may also be interested in the Mortgage Solutions newsletter. All the latest news, analysis and insight from the mainstream residential lending market. Including industry news, adviser business strategy tips and market commentary.