Better Business

How to rescue a failing business – Flavin

Guest Author:

Paul Flavin, business growth specialist at Grow PartnershipRunning a small business can be tough and definitely comes with its own set of challenges.

To survive, you need to understand the four key pillars of business, starting in this case with finance. This means knowing how to manage cash flow and get funding. You’ll also need to have a clear understanding of the other three pillars: marketing, sales and operations.

This guide is here to offer practical tips and ideas. It aims to help struggling businesses spot problems, look for answers, and find a way to recover.

Diagnosing your business health

Every business owner should check the health of their business regularly, just like attending a doctor’s visit. This means looking closely at different parts of the business. These parts could include financial status, how happy customers are, where the business stands in the market, and how well it is running.

If you ignore the signs of a failing business, it can cause serious problems. Finding issues early is very important for a good recovery. Noticing these signs and acting quickly can help in using successful turnaround strategies.

Aldermore Insights with Jon Cooper: Edition 10 – The biggest barrier to homeownership isn’t affordability. It’s outdated lending.

Sponsored by Aldermore

Identifying the symptoms of a failing business

One clear sign of failure is a repeated pattern of late payments from customers. This can cause negative cash flow. It makes it hard to pay for costs like rent, utilities, salaries, and invoices from suppliers. Without enough cash flow, businesses may find it hard to meet their bills. This can make the situation worse.

Another sign to watch for is falling sales and unhappy customers. This might happen for many reasons. There could be more competition, changes in what buyers want, or drops in product or service quality.

If these issues are not fixed quickly, they can grow into bigger problems. You may end up with rising debt, legal trouble, or even closing the business. So, it is very important to see these warning signs early and take action to solve the issues.

Conducting a financial audit: cash flow and debt analysis

A thorough financial audit is a good first step to understanding your situation better.

Start by looking at your cash flow statements, bank account transactions, and pending debts. Try to spot any overspending, loss of income, or trouble in getting payments.

After you get a clear view of your finances, think about getting outside financial support. You can talk to your bank or check out other funding options, like government grants or business loans.

It’s important to act early. The faster you spot and fix financial problems, the better your chances for a successful turnaround.

Strategic planning for recovery

Once you know the main reasons behind your business problems and have a good grasp of your finances, it’s time to create a plan to recover. This plan should set clear goals, focus on important actions, and adjust to the changing business world.

A solid plan works like a compass. It helps you make decisions and keeps all your efforts focused on one main goal: saving your business from failing. You need to be honest, flexible, and committed to ongoing check-ups and improvements.

Setting clear, achievable goals

When you want to bring a struggling business back to life, it is very important to set clear and realistic goals. This is the first step to recovery and business growth. Your goals need to be specific, measurable, attainable, relevant, and time-bound, or SMART.

Instead of trying to fix everything at once, focus on small improvements that you can achieve in a set time. Break large goals into smaller tasks. This way, you can easily track your progress and celebrate small wins along the way.

The key is to target actions that will make the biggest difference and help your business last for a long time.

Prioritising actions based on impact

An effective turnaround strategy starts with really knowing your target market. It also involves focusing on actions that matter most to your business. Rather than trying to fix everything all at once, choose the areas that will bring the best results.

For instance, if you’re worried about keeping customers, make customer service, loyalty programmes, or focused marketing campaigns your top priority. By investing in yourself as a business owner, like through mentoring or a management course, you can learn important skills and gain knowledge.

When you focus on actions that match your business goals and meet the needs of your target market, you will be able to create positive change more easily.

Optimising operations to reduce costs

In tough financial times, it is important to find ways to cut operational costs while still delivering good service.

Many businesses find they can automate some tasks or outsource them, leading to big savings.

Streamlining processes for efficiency

Take a close look at how your team works now. Find any problems or places where things slow down. These issues can waste time and money. Using tools like accounting software for invoices can help your team work better. They can also lower the chance of mistakes.

It’s important to have clear ways for your team to talk to each other. This helps everyone know what is happening. Holding team meetings and sharing updates keeps things open and accountable.

By always checking and improving your business methods, you can save money. This will help you build a team that can change as needed. Plus, regularly predicting your financial needs helps you manage money better.

Boosting sales and marketing efforts

Cost optimisation is important, but that doesn’t mean you should ignore ways to increase sales and marketing. You might want to look at your pricing strategy again. Try finding new marketing channels to reach more people. You could also create special promotional campaigns.

In a market with a lot of competition, it’s important to remind customers what makes your business special. Offer them incentives that make them want to choose you.

Remember, it’s far easier to grow your way out of financial duress than it is to save your way out. There’s a finite amount of savings that can be made but no real cap to your sales increase.

Re-evaluating your target market

Changes in market trends, the economy, and what customers want can seriously affect your business success. Doing good market research helps.

This is true even if your business is mostly online. It makes sure what you offer fits well with your target market. You can gather customer feedback through surveys, online reviews, or by talking directly to them. This way, you learn about their changing needs and preferences.

Look again at who your ideal customer is. Pay attention to any shifts in their age or buying habits. This will help you improve your marketing messages, adjust your products or services, and find new opportunities in your niche.

If you keep adjusting to the changing market and focus on what customers need, you will set your business up for growth, even when the economy is unsure.

Implementing cost-effective marketing strategies

When money is tight, it’s very important to be clear in your marketing message. You also need to deliver this message effectively to your audience.

The good news is there are many low-cost strategies for businesses working on a budget. You can use social media, email marketing, and a company blog to reach a lot of people without spending too much.

Partnering with businesses that offer different products can help you reach more customers. You can also join local events or trade shows to meet potential buyers directly. Find who has access to your ideal clients before you do then discuss some form of partnering.

Keep in mind that marketing doesn’t need to cost a lot to be effective. By using focused strategies and improving your efforts, you can attract new customers, boost sales, and help your business grow.

Financial restructuring and funding options

In addition to making operations better, looking into financial restructuring options can really help a struggling business.

Also, checking out different ways to get funding, like government grants, business loans, or equity financing, can give the money needed to improve operations and chase growth opportunities.

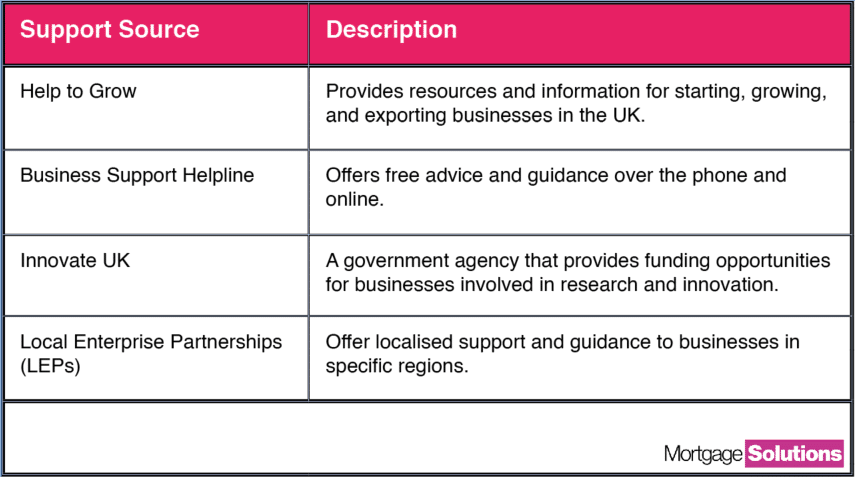

Exploring government grants and loans in the UK

When facing financial difficulties, investigating government support programmes can be a game-changer.

The UK government offers a range of grants and loans specifically designed to assist businesses. These schemes, often managed through HMRC and other agencies, provide financial aid for various purposes, such as research and development, innovation, exporting, and regional development.

Remember, eligibility criteria and application processes vary for each programme. It’s essential to carefully review the details and seek guidance if needed. These government-backed finance options can provide a much-needed boost.

Conclusion

In conclusion, saving a failing business needs a smart plan.

First, you should identify the problems. Next, set realistic goals. Then, improve how things run and increase sales. It’s also important to look at finances and find ways to get funding. This can help bring in the money needed for recovery.

By taking action and making good choices, businesses can get through tough times and aim for both stability and growth. Don’t forget, asking for professional help and exploring all the options is crucial for helping a struggling business.